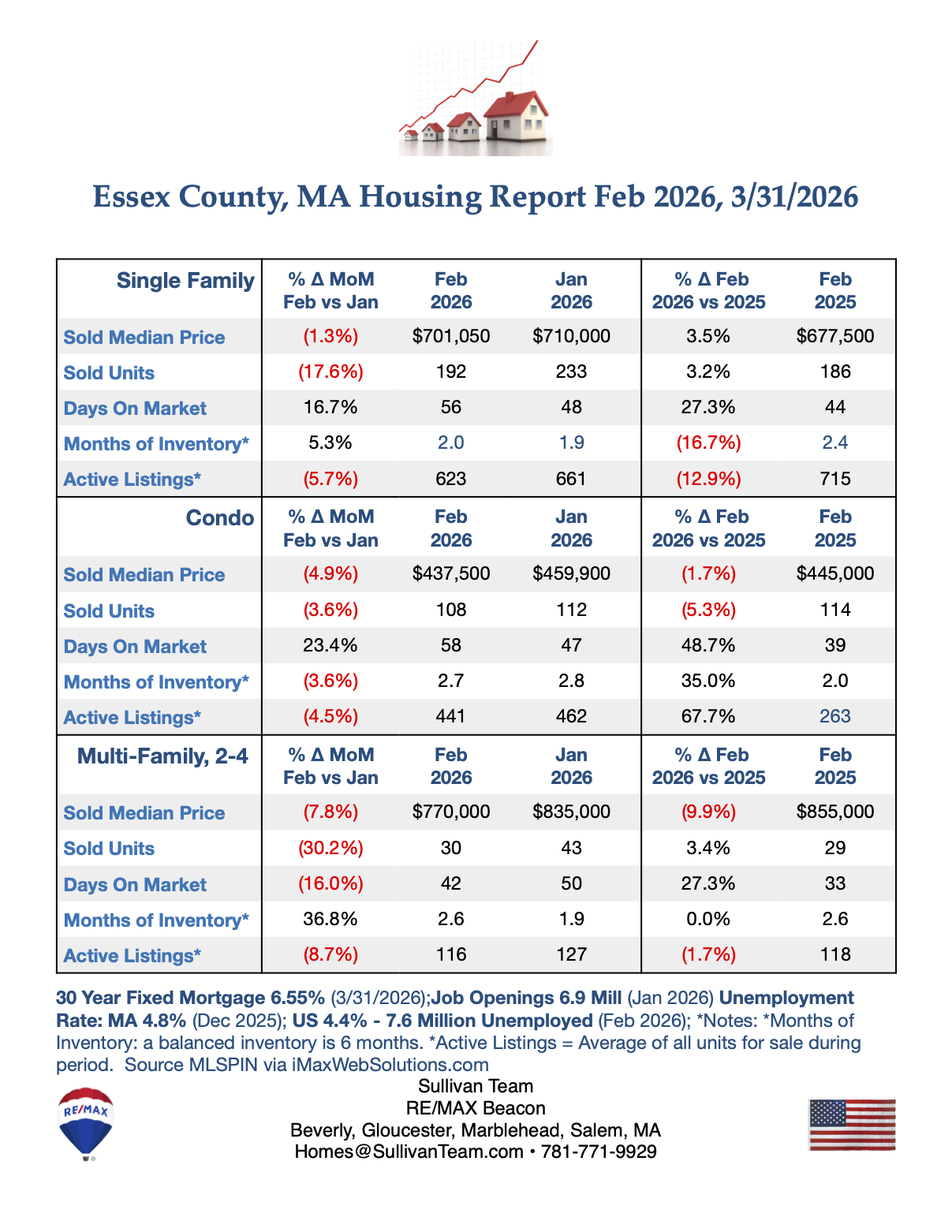

Housing Report Feb 2026 vs Jan 2026, 3/31/2026

National Report: Homes (Single Family Homes and Condos)

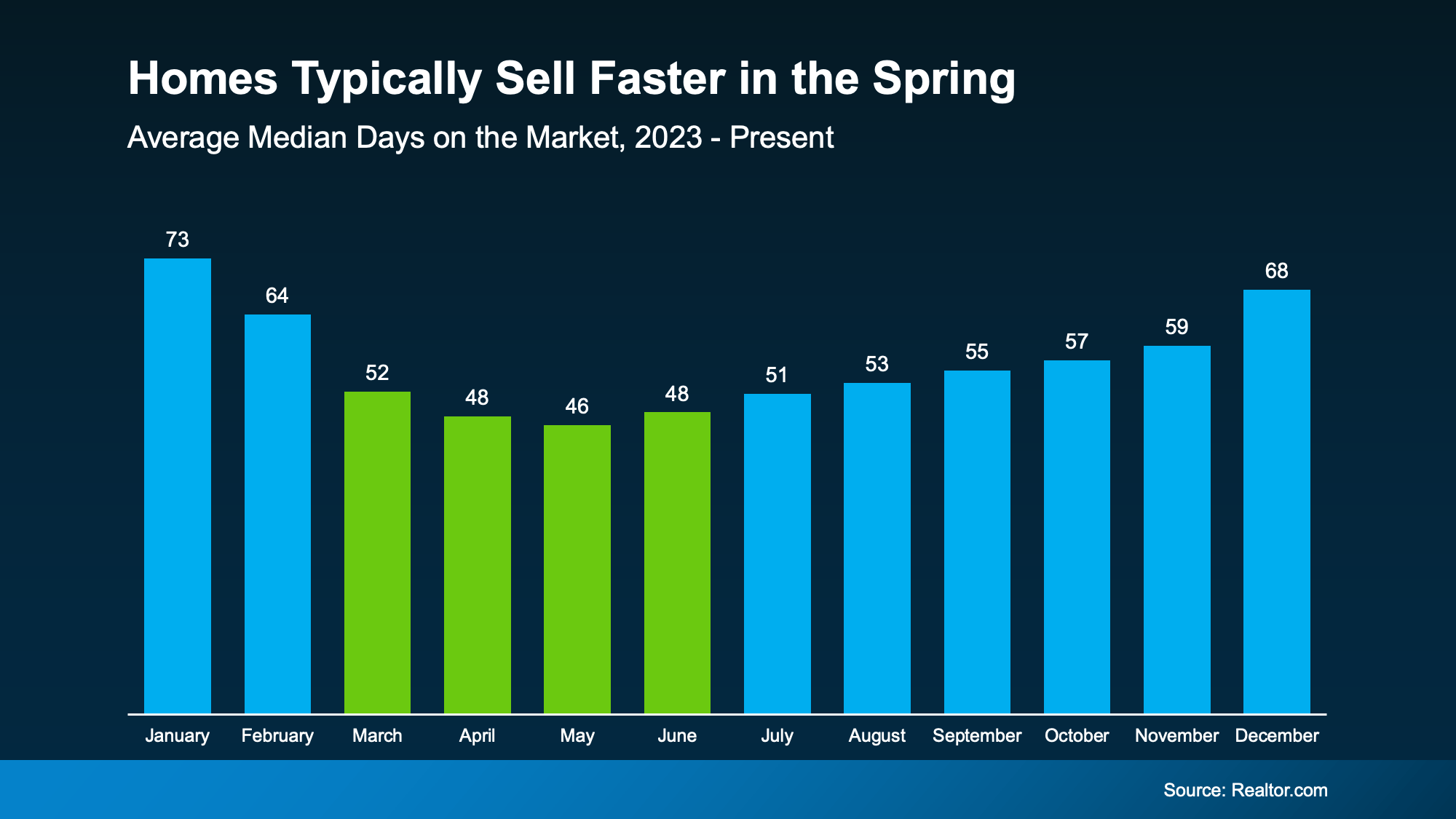

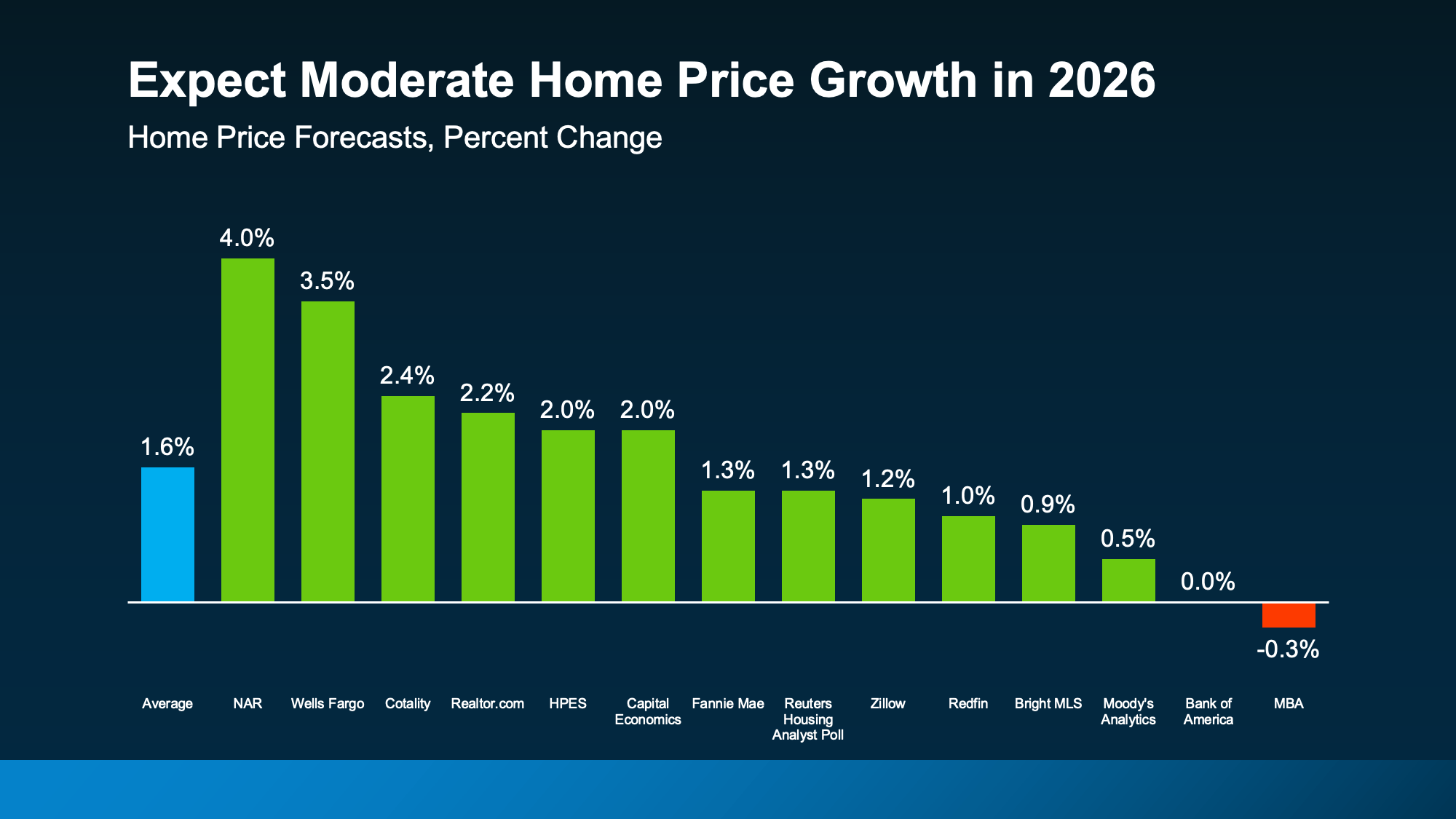

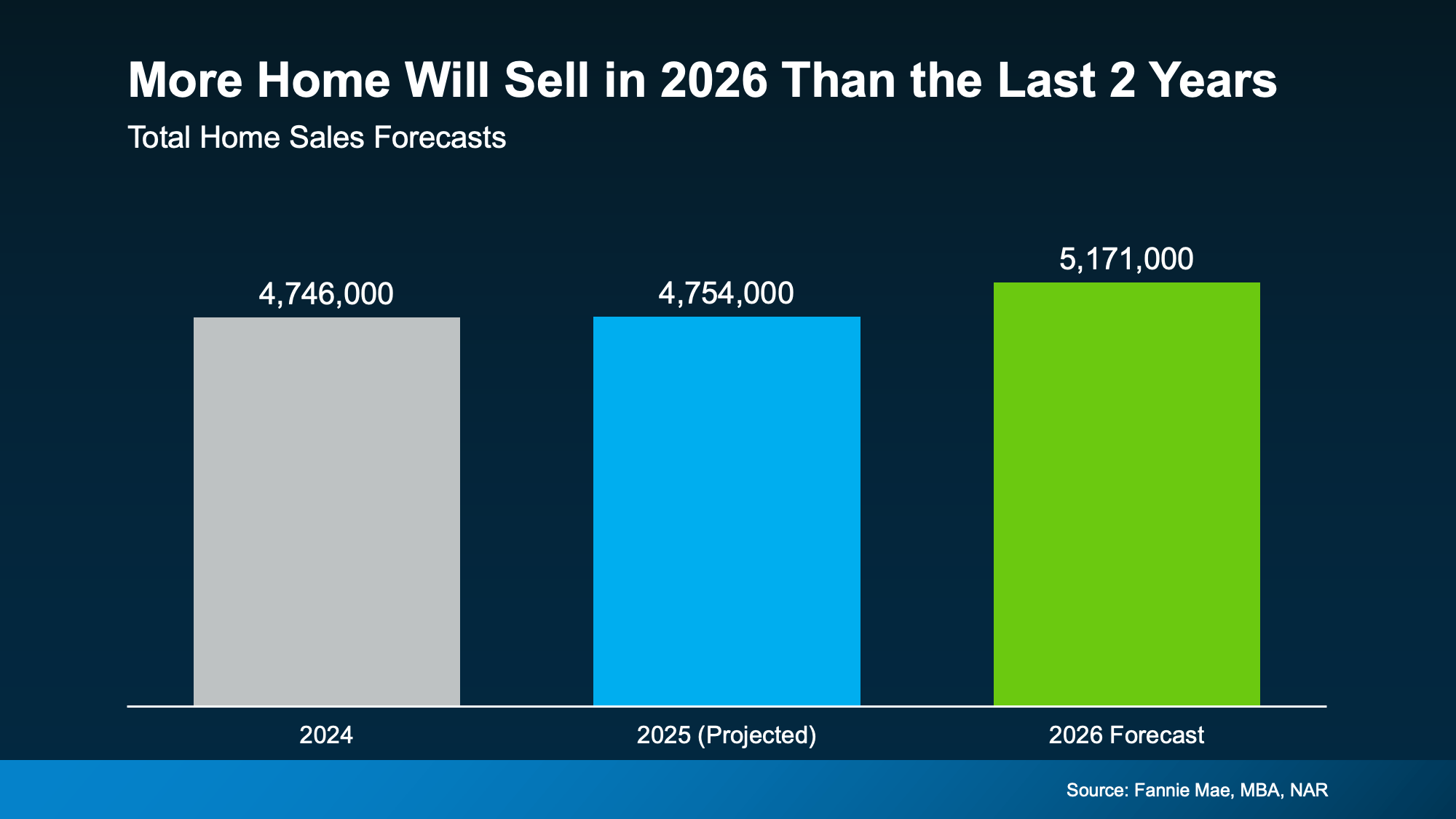

The number of homes sold rose 1.7%, median sold prices rose 0.8% to $398,000 and days on market rose 2.2% to 47 days. 15.8% of February’s active listings had a price reduction, the sale-to-list-price ratio was unchanged at 98% and inventory was unchanged at 3.8 months.

Bottom Line: The market is becoming more balanced between sellers and buyers as prices flatten, and inventory and days on market are rising.

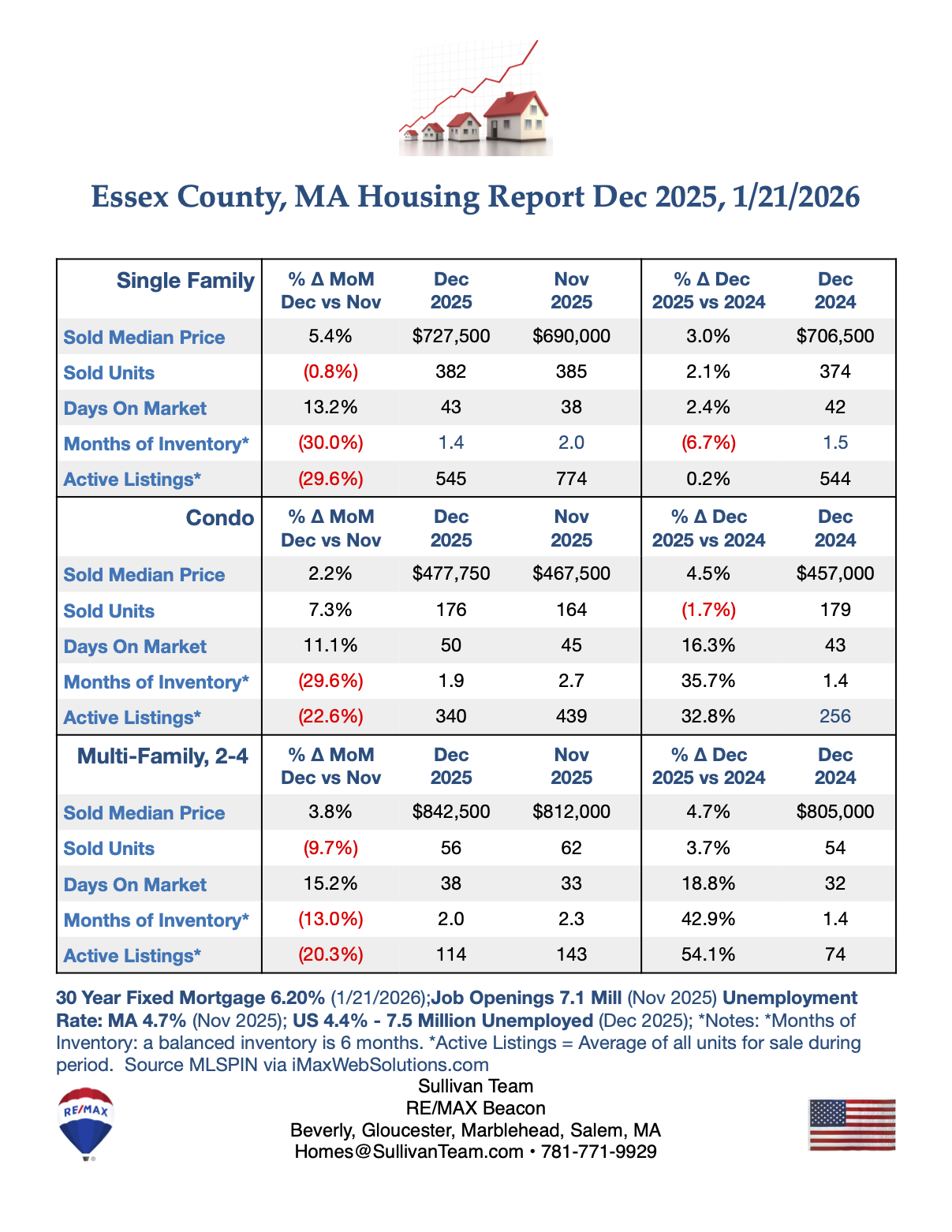

Essex County - Feb 2026. vs Jan 2026., Winter took its toll:

Unit Sales were down -17.6% for single-family and -3.6% for condo; Prices fell -1.3% for single-family and -4.9% for condo. However, inventory remained very low: single-family 2.0 months and condo 2.7 months. 10.6% of single-family listings and 10.3% of condo listings had price reductions in February which averaged -3.9% and -2.9% respectively. The sale-price-to-list-price ratio for single-family and condo was 99%.

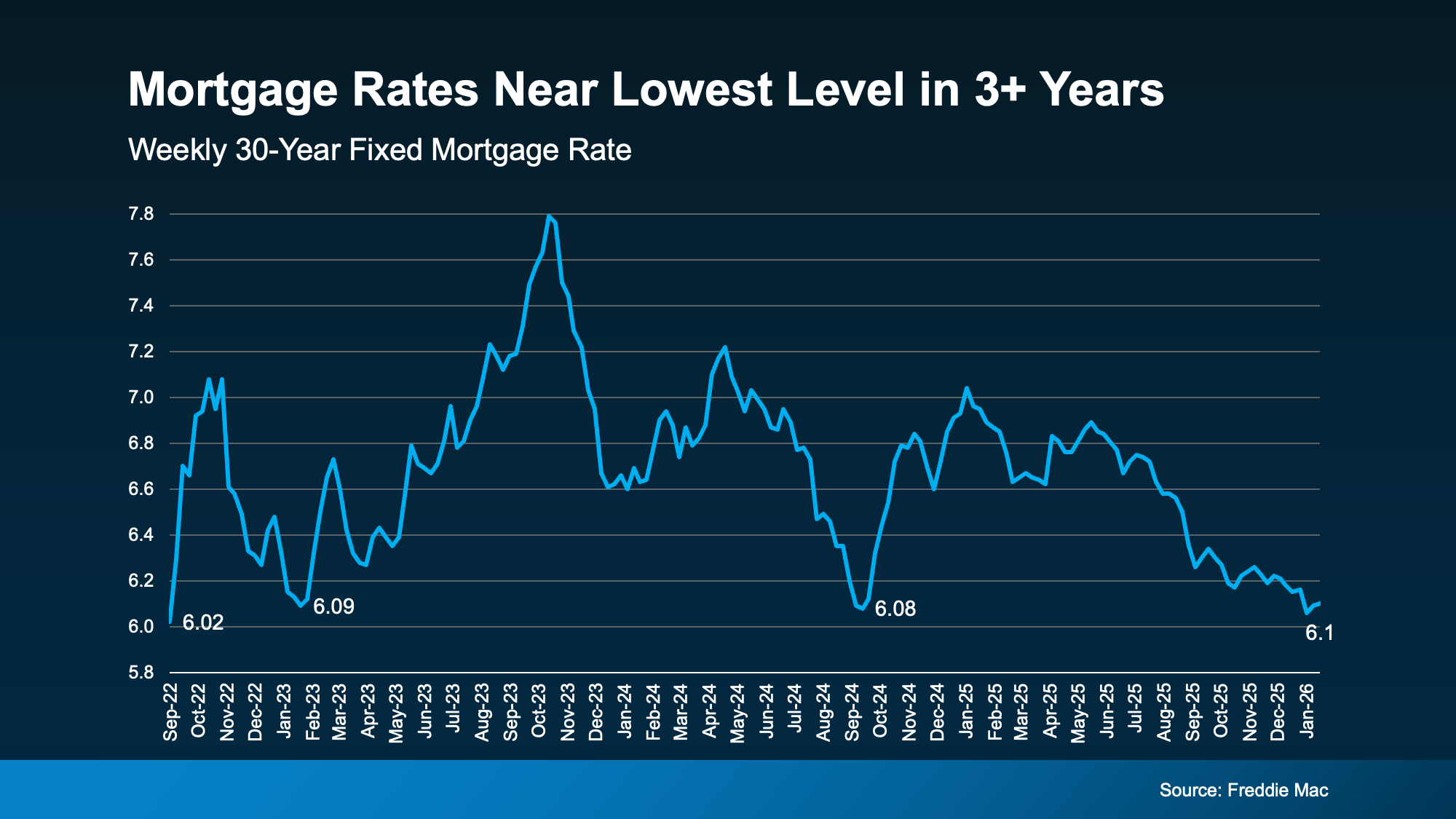

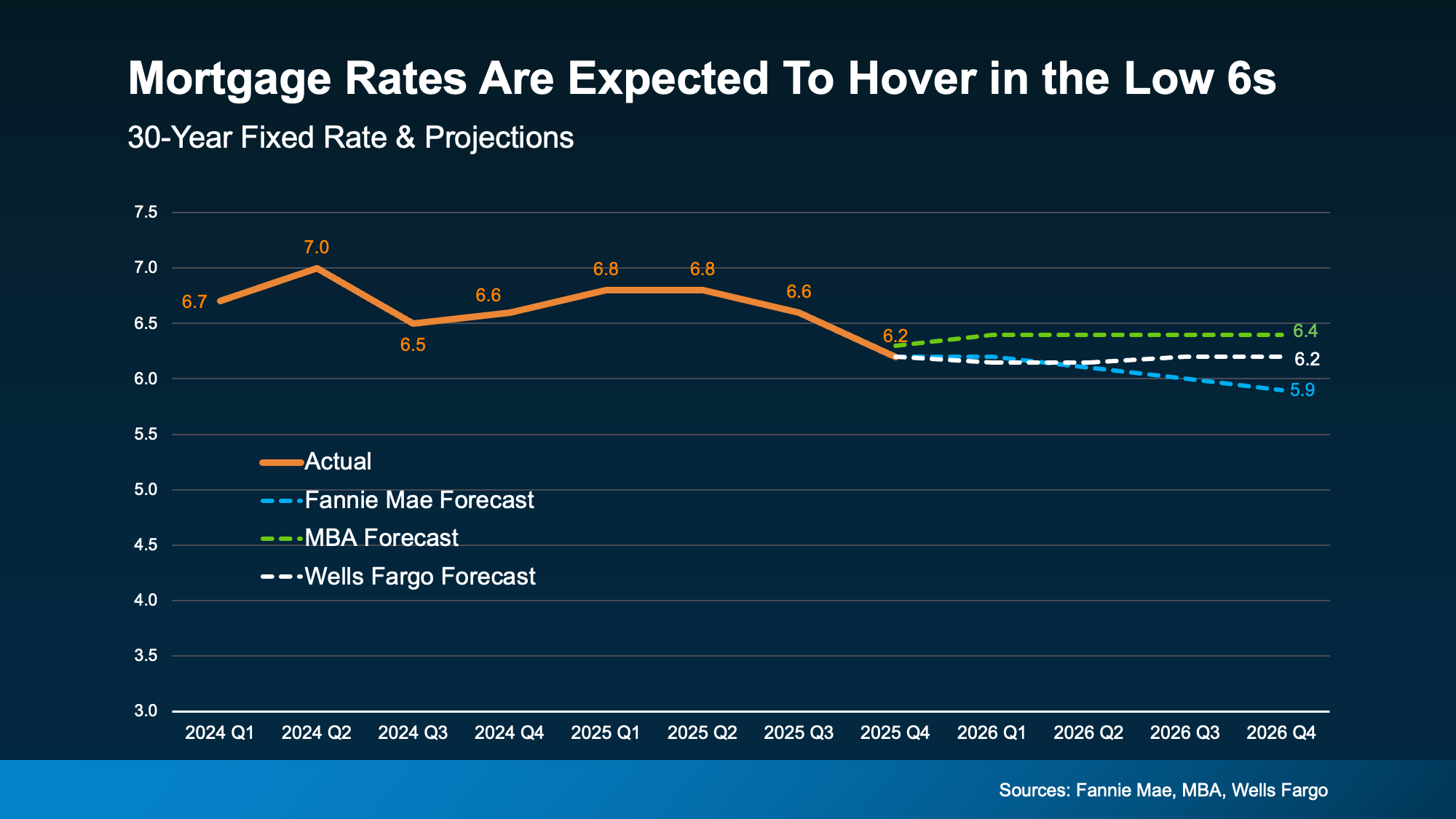

Bottom line: very low inventory still favors sellers but buyer price resistance is having an impact. A new challenge is the ½% rise in mortgage rates to 6.55% from the end of Feb to the end of March.

To view data for every Essex County town,

- To view data for every Essex County town, http://www.sullivanteam.com/Properties/Reports/Public/Charts.php

- To Download the full housing report go to: http://sullivanteam.com/pages/EssexCountyHousingReports